The Climate-Nature Nexus in Practice (Issue to 06 June 2026)

Nature lost track of its own size: The constraint is no longer whether nature is investable, but whether any figure survives being quoted twice.

Nature is an asset class that can’t agree on its own size

Issue to 06 June 2026 - No. 2

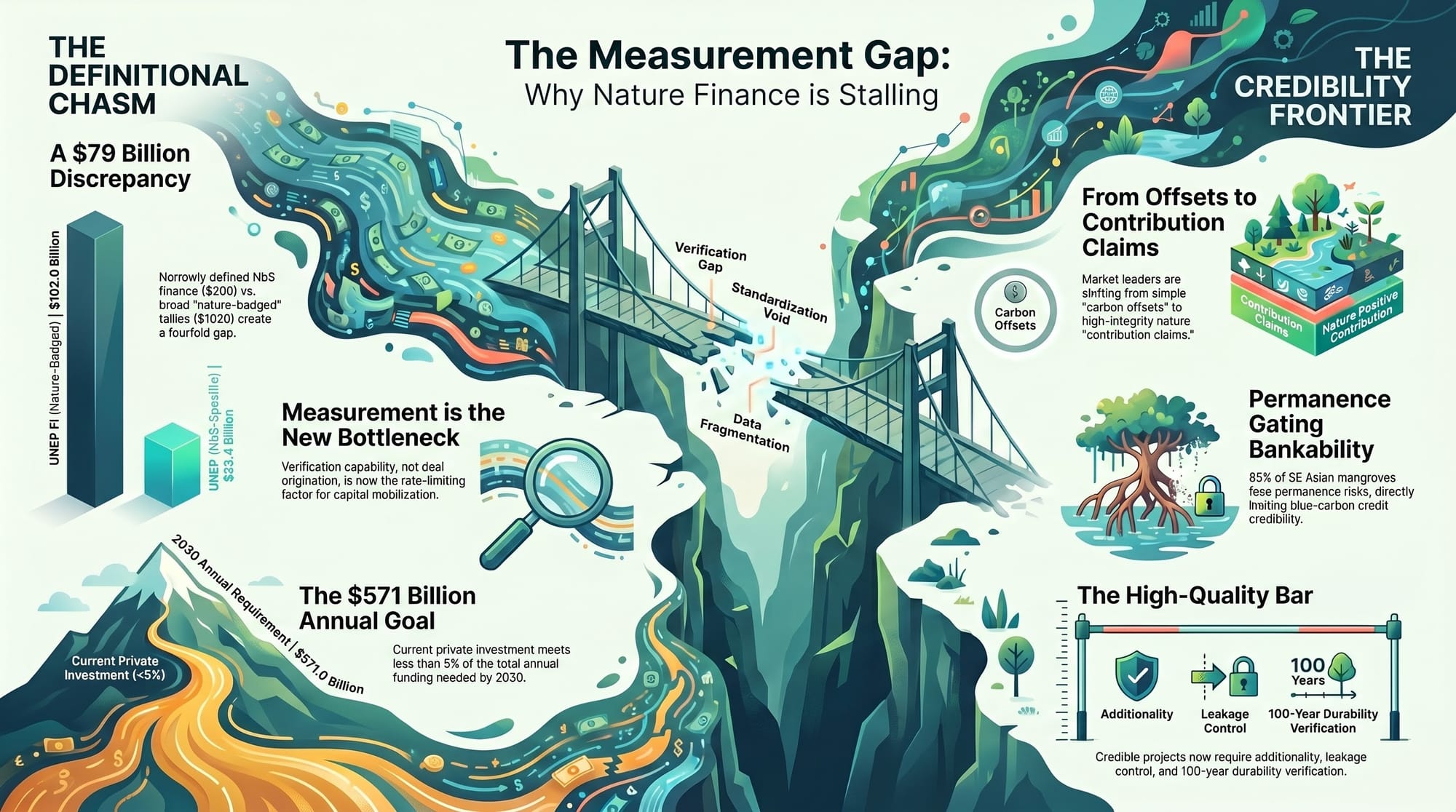

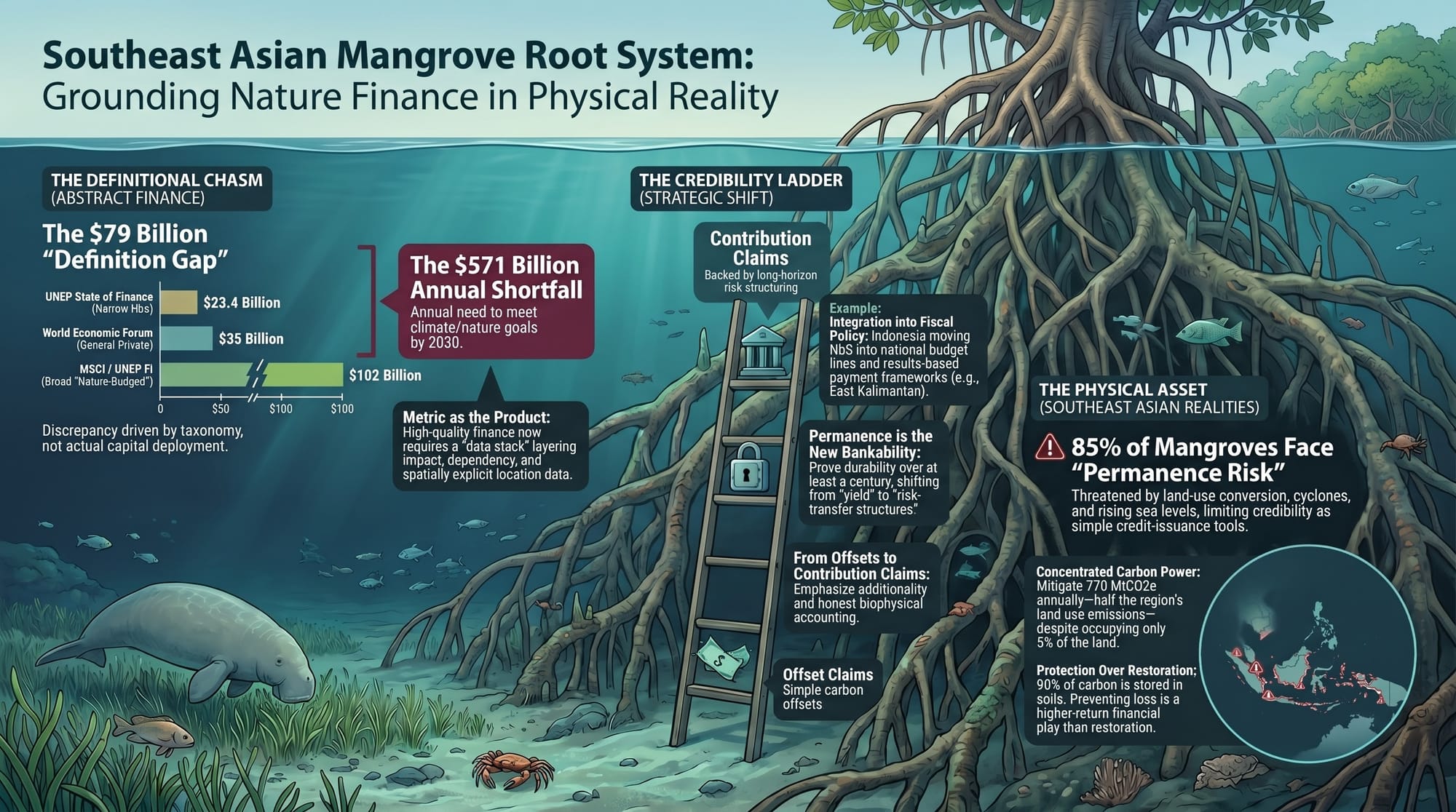

Bottom line: Nature became an asset class last week; this week it lost track of its own size. UNEP’s State of Finance for Nature 2026 counts roughly $23 billion in private NbS finance, while the headline “nature-badged” tally counts $102 billion, a fourfold discrepancy between two UN sources for the same year. A number that swings that far is not a measurement; it is a confession. The constraint is no longer whether nature is investable, but whether any figure about it survives being quoted twice. Stop selling the category. Start selling the proof.

Here is the door into the field, and the briefing is the room you walk into: [Podcasts and Video — NotebookLM ]

Link to Explainer Video

Last week, this briefing argued that nature finance had graduated from advocacy to an asset class and that the binding constraint had shifted from legitimacy to assurance. This week sharpens and deepens the diagnosis: the problem starts before verification because the field cannot agree on how much money is already in the room. On 5 June, World Environment Day wrapped nature and climate in a single banner, while the UN Secretary-General quietly conceded that a temporary overshoot of 1.5°C is now almost inevitable, given that the past 11 years are the hottest on record.[1] The loudest document of the week, though, was not a speech. It was a spreadsheet.

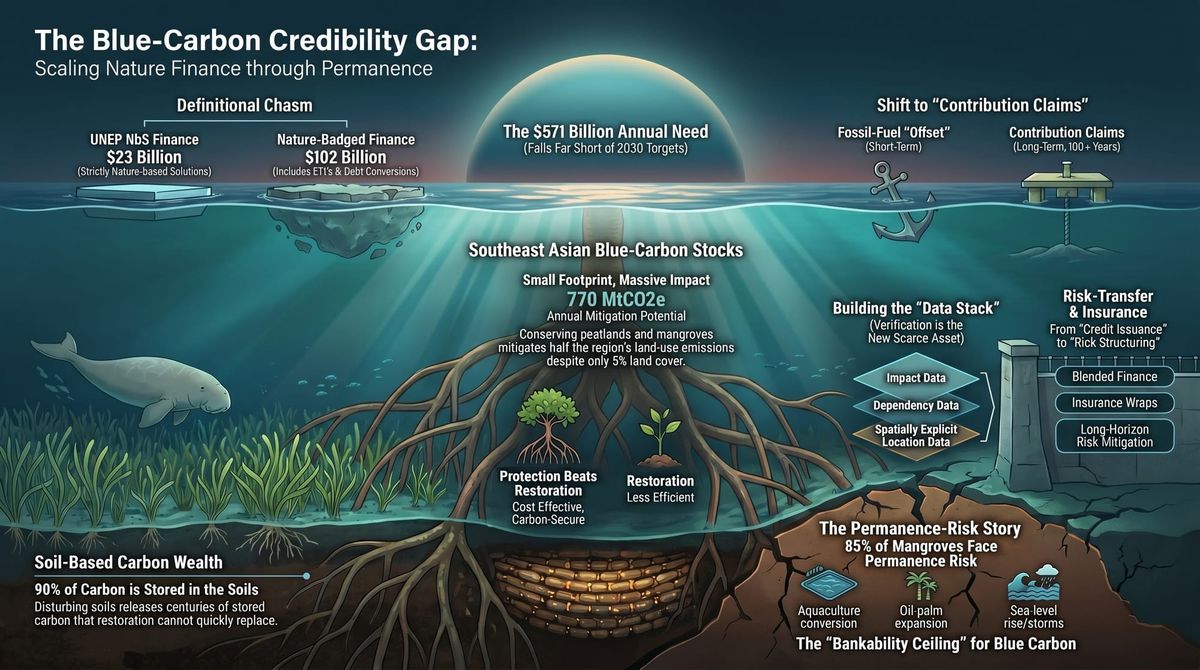

UNEP’s State of Finance for Nature 2026 estimates private finance for nature-based solutions at about 23 billion dollars in 2023, against a need approaching 570 billion a year by 2030, with public money still carrying 90% of the load.[2] Set that beside the figure every investor deck quotes, the “nature-badged” tally near 102 billion, the very number this briefing dissected last week.[3] Same year, same planet, two UN-affiliated sources, a fourfold gap. They are not contradicting each other; they are counting different things, with one measuring NbS narrowly and the other sweeping in every nature-labeled instrument, from biodiversity ETFs to debt swaps. But a headline that quadruples depending on which taxonomy you pick is not a market size. It is an admission that the field still lacks a shared, decision-grade definition of what it finances.

For senior practitioners, the lesson builds on last week’s. The scarce skill is not finding deals or even verifying them; it is producing numbers that hold up when others quote them. That means adding a definition and a provenance caveat to every figure you publish and treating measurement as infrastructure rather than as reporting. The rest of the week says the same thing from downstream: green bonds that still cannot prove they are green, and Southeast Asian mangroves that cannot promise to remain standing. Capital has decided that nature is an asset class. It has not decided which nature to trust. That gap is the whole opportunity.

The Number That Won’t Hold Still

The contest in nature finance has quietly shifted from raising capital to making capital legible. Four shifts are now visible, and each one rewrites a practitioner’s job description.

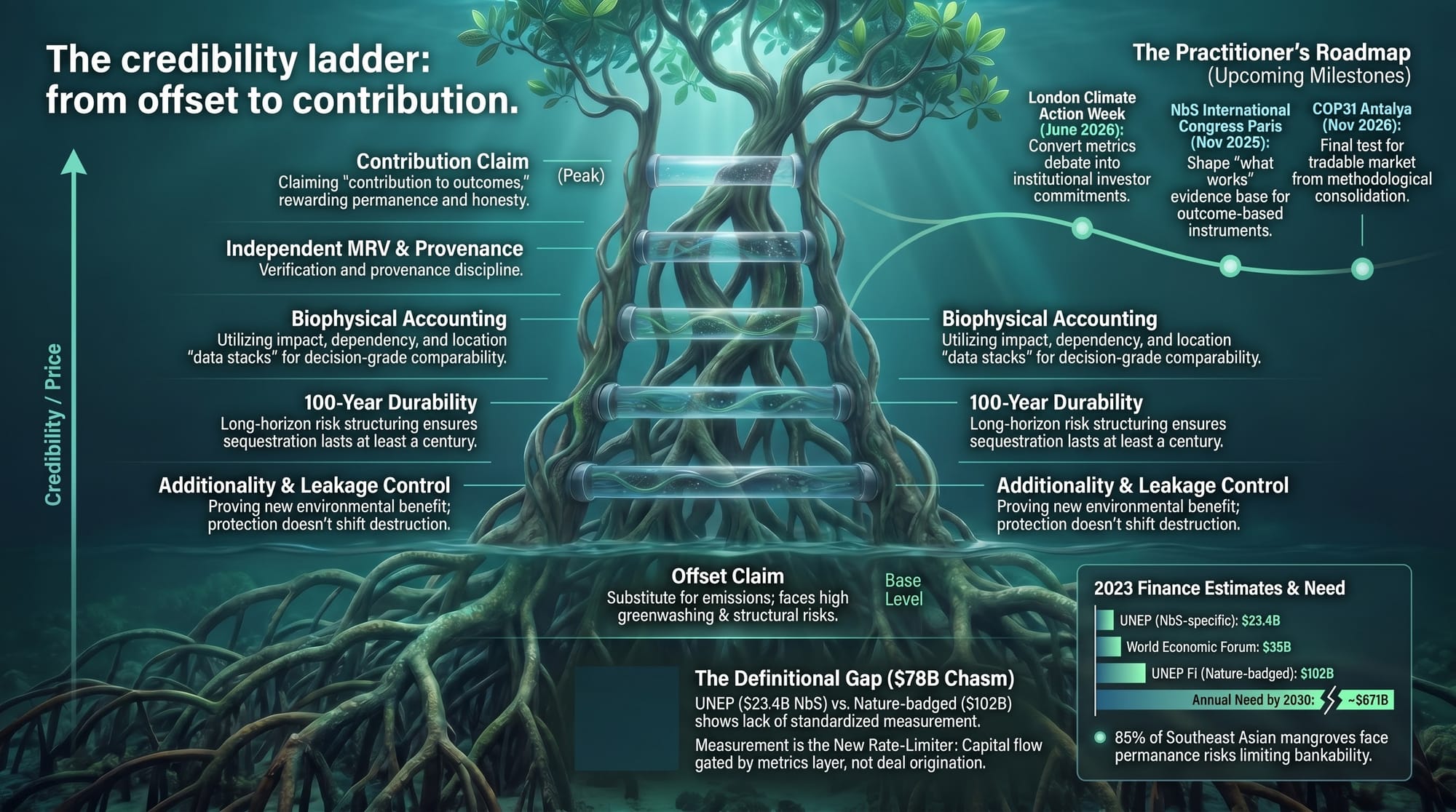

Start with the number that won’t sit still, because it explains the rest. Depending on where you draw the line, private finance for nature in 2023 was 23, 35, or 102 billion dollars.[4] A fourfold among credible sources is not a curiosity; it is a market failure the sector is finally trying to price. The Taskforce on Nature-related Financial Disclosures and the “data stack” logic in NatureFinance’s investor guidance, which stacks impact, dependency, and location data, are bids to give nature the decision-grade comparability carbon won a decade ago.[5] November’s Paris NbS Congress has built a third of its sessions around “what works,” a polite way of admitting the field skipped that step. The scarce asset now is verification, not origination.

The second shift is the slow death of offsetting. A net-cooling roadmap for nature-based climate solutions tightens the screws on additionality, leakage, century-scale durability, and honest biophysical accounting, until the only defensible corporate sentence left is “we contributed,” not “we offset.” [6] While the synthesis in Science is blunt, such solutions complement, but never replace, cutting fossil fuels.[7] That is not wording. It reprices the credit, raises the bar for issuers, and rewards the project that can prove permanence rather than the one that merely claims sequestration.

The third shift drags NbS and EbA out of the pilot column and onto the balance sheet. EU Green Week now discusses nature finance “across the budget lines,” and the NAP Global Network continues to document ecosystem-based adaptation written directly into national plans and into agriculture, water, and city budgets. [8] The unit of engagement is shifting from the orphan concept note to the national plan and the portfolio, meaning the buyer is now the finance ministry, and the product is a pipeline aligned with a nationally determined contribution (NDC).

The fourth shift is the one generalist capital keeps underpricing: permanence is now the binding constraint on bankability. Where a mangrove sits matters as much as how the deal is structured, because roughly 85% of Southeast Asia’s mangroves face some risk of permanent loss from conversion, cyclones, and rising seas that no credit can paper over.[9] Durability, not yield, separates a bankable coastal structure from a stranded one. “Bankable NbS” increasingly means long-horizon risk engineering, layered blends, insurance wraps, and protection over restoration, not a tidy issuance story.

Follow the logic, and three things follow. Protection finally out-earns restoration because keeping a peatland intact costs a fraction of what it takes to rebuild a drained one and preserves centuries of buried carbon. Results-based payments and Indonesia’s East Kalimantan template live or die on whether domestic budgets continue to pay once the donor stops.[10] With the United States walking out of the Paris Agreement and the $1.3-trillion-a-year Belém roadmap left to everyone else, private and blended capital matter more, not less, making the metrics that govern them the real fight. COP31 in Antalya in November will show whether any of these consolidations produced something the market can trade.[11]

The Record

Conviction and capital both showed up this week. Agreement on the basic arithmetic did not. Each item is read for what it does to that gap.

World Environment Day put the nexus center stage, and the Secretary-General admitted the overshoot. The UN’s biggest environmental day fused nature and climate, even as the Secretary-General acknowledged that a temporary 1.5°C breach is now near-certain and that the last 11 years have been the hottest on record. The framing is a win: the integration we have argued for is now the UN’s headline. But attention is not money, and this day moved attention. UN Environment Programme, 5 June 2026. Global; Baku commemoration. https://www.unep.org/news-and-stories/press-release/planet-swelters-world-environment-day-2026-focuses-urgent-climate

UNEP’s own ledger says $23 billion. Everyone else says $102 billion. The State of Finance for Nature 2026 reports about $220 billion in total NbS finance in 2023, with barely $23.4 billion of it private, and roughly 90% public, against a $571-billion-a-year need by 2030, with growth limping at 5%. It is the most rigorous public count we have and belongs at the top of the evidence stack; its narrow NbS boundary is exactly why it sits at a quarter of the size of the “nature-badged” headline. Compiled from public flows, not audited at the project level. UNEP, State of Finance for Nature 2026: “Nature in the Red.” Global. https://www.unep.org/resources/state-finance-nature-2026

Green bonds still can’t prove they’re green. A peer-reviewed study finds that green bonds do channel money to environmental projects, but some add little beyond plain vanilla debt, the textbook definition of greenwashing.[12] For nexus vehicles, the moral is clear: the label is a decoration unless use of proceeds, project selection, and post-issuance reporting include real nature metrics and safeguards. Evidence established in 2024 is now cited more often as taxonomies absorb nature criteria. Humanities and Social Sciences Communications (Springer Nature), 2024. Global. https://www.nature.com/articles/s41599-024-04318-1

EU Green Week moved NbS from the pilot line to the budget line. Two official partner events reframed nature-based solutions as something to bake into public budgets and insurance, rather than fund as one-off pilots. The venue signals that NbS finance is entering the EU fiscal conversation, where durable scale actually comes from, though no euros are attached yet. NATURANCE and partners, EU Green Week 2026 (Brussels, 2 June; Athens, 23 June). European Union. https://www.naturanceproject.eu/nature-based-solutions-naturance-eu-green-week-2026/

From offsetting to contribution: the proof bar just went up. A net-cooling roadmap pushes corporates away from offsetting and toward contribution claims, demanding additionality, leakage control, century-scale durability, and biophysical honesty, [6] while the Science synthesis insists that nature complements rather than decarbonizes.[7] Together, they reprice NbS credits around permanence, not volume. The open question is whether voluntary markets adopt the harder logic before it stops mattering. University of Utah roadmap; Science (AAAS) synthesis. Global. https://attheu.utah.edu/research/carbon-offsets-arent-working-heres-a-way-to-fix-nature-based-climate-solutions/ https://www.science.org/doi/10.1126/science.abn9668

ASEAN in Focus

Southeast Asia hosts the world’s most efficient carbon sinks and an outsized share of its permanence risk, making it the test of whether blue carbon can be durable or only issued.

Southeast Asia is where the measurement problem becomes a balance-sheet problem. New peer-reviewed work finds that protecting and restoring the region’s peatlands and mangroves could cut roughly 770 megatons of CO₂-equivalent emissions a year, about half its land-use emissions, from ecosystems covering 5% of its land, with over 90% of the carbon locked in soil; the ASEAN Peatland Management Strategy 2023–2030 sets the policy frame.[13] The uncomfortable corollary: about 85% of the region’s mangroves face permanence risk from oil palm, rice, aquaculture, cyclones, and sea-level rise, which caps how far blue-carbon credits can finance their protection.[9] So protection beats restoration because a drained peatland releases centuries of carbon, and durability, rather than yield, determines which coastal deal is bankable. April’s ASEAN Climate Week, under the Philippine chair, pushed “from ambition to delivery” and named mangrove, seagrass, coral, and watershed restoration as adaptation infrastructure [14] while a recent AIT webinar on NbS in ASEAN cities showed how far urban pipelines still sit from finance.[15] The opportunity is genuine; governance, tenure, and verification, not the science, will decide whether it is ever realized.

Worth Watching Through Year-End

The diary through December is full of convenings that set standards and shape pipelines, not conferences that write checks, proof that the field is still debating how NbS should be measured. Watch the standards, not the headlines.

London Climate Action Week & the UNEP FI Global Roundtable — 20–28 June 2026, London. Europe’s largest climate festival (≈45,000 people), featuring the UNEP FI Roundtable on “risk to resilience: financing the future.” The nearest venues to turn the measurement argument into actual commitments are the nature-finance and resilience rooms. E3G; UNEP FI. https://londonclimateactionweek.org/

EU Green Week financing-NbS session — 23 June 2026, Athens. A focused session on the budgetary plumbing for NbS and biodiversity restoration, a concrete door into the EU’s effort to fold nature spending into public finance. NATURANCE and partners. https://www.naturanceproject.eu/nature-based-solutions-naturance-eu-green-week-2026/

Climate Week NYC — 20–27 September 2026, New York. The year’s largest corporate-and-government gathering, beside the UN General Assembly, where contribution-claim strategy meets reality, is the bellwether for whether the offset-to-contribution turn is real or theater. Climate Group. https://www.climateweeknyc.org/news/climate-week-nyc-returns-september-2026

NbS International Congress 2026 — Paris, 3–6 November 2026. The principal NbS knowledge exchange, 33 sessions on evidence, finance structuring, and Article 6; expect advances in monitoring and verification, not disbursements. Biodiversa+. https://www.biodiversa.eu/2026/05/05/nature-based-solutions-international-congress-2026/

UNFCCC COP31 — Antalya, Türkiye, 9–20 November 2026. Amid Belém’s $1.3-trillion goal and the US's Paris exit, the multilateral anchor will set the policy envelope for NbS and EbA through its Article 6, adaptation finance, and forest workstreams. UNFCCC — Türkiye presidency, Australia leading negotiations. https://unfccc.int/cop31

ENDNOTES

[1] World Environment Day 2026, UN Environment Programme; host Azerbaijan (Baku); UN Secretary-General’s message on the eleven hottest years and a likely temporary 1.5°C overshoot, 5 June 2026. Primary (UNEP); current-week observance, not a finance event. https://www.unep.org/news-and-stories/press-release/planet-swelters-world-environment-day-2026-focuses-urgent-climate

[2] UNEP (2026). State of Finance for Nature 2026: Nature in the Red — Powering the Trillion-Dollar Nature Transition Economy. Figures (~$23.4bn private NbS finance and ~$220bn total in 2023; ~90% public; ~$571bn/yr need by 2030) as reported and summarized in Nature4Climate’s review (14 April 2026). Compiled from public flows and reported transactions, not project-level audit; NbS-specific boundary, narrower than “nature-badged” tallies. https://www.unep.org/resources/state-finance-nature-2026

[3] MSCI (2024). The Climate–Nature Nexus: A Primer on the Way to Cali. The $102bn “nature-badged” figure originates with UNEP FI, “Private finance for nature surges to over $102 billion” (Dec 2023 research; page June 2024). Member-reported / compiled, no standardized taxonomy; directional, not current-week. https://www.msci.com/research-and-insights/blog-post/the-climate-nature-nexus-a-primer-on-the-way-to-cali

[4] World Economic Forum (2025). Nature-finance models / Finance Solutions for Nature — cited for the ~$35bn private estimate and the ~$2.7tn/yr nature-positive need, illustrating the spread of figures across differing boundaries. Compiled; differing definitional boundary. https://www.weforum.org/stories/2025/09/nature-finance-sustainable-investing-priority-models/

[5] NatureFinance (F4B) with UNEP-WCMC (2022). Climate–Nature Nexus Investor Guide — the “data stack” approach, TNFD-aligned. Established 2022 methodology; mainstream-portfolio uptake still lags. https://www.naturefinance.net/

[6] University of Utah, roadmap for nature-based climate solutions that deliver net global cooling (additionality, leakage, century-scale durability, biophysical accounting; offset → contribution). University research communication. https://attheu.utah.edu/research/carbon-offsets-arent-working-heres-a-way-to-fix-nature-based-climate-solutions/

[7] Synthesis on the benefits and limits of nature-based solutions, Science (AAAS). Peer-reviewed synthesis; foundational reference, not breaking news. https://www.science.org/doi/10.1126/science.abn9668

[8] NAP Global Network (IISD). Ecosystem-based adaptation in national adaptation plans and sectoral planning. Network guidance: Country uptake is uneven. https://napglobalnetwork.org/themes/nature-based-solutions/

[9] Socioeconomic and climate-change permanence risks affecting ~85% of Southeast Asian mangroves, Communications Earth & Environment (2025). Peer-reviewed; 2025. https://www.nature.com/articles/s43247-025-02035-4

[10] World Bank, East Asia and Pacific — Indonesia East Kalimantan Emission Reductions Payment Agreement (performance-based forest payments). Program example: durability and benefit-equity are uncertain once payments cease. https://www.worldbank.org/en/region/eap/brief/the-abcs-of-climate-action-in-east-asia-and-pacific

[11] COP31, UNFCCC, Antalya, Türkiye, 9–20 November 2026 (Türkiye presidency; Australia leading negotiations). Backdrop: COP30 Belém $1.3-trillion/yr-by-2035 mobilization goal; US withdrawal from the Paris Agreement effective early 2026. Multiple sources; procedural details provisional pending the official COP31 page. https://unfccc.int/cop31

[12] Green-bond dual-impact and greenwashing study, Humanities and Social Sciences Communications (Springer Nature), 2024. Peer-reviewed; 2024 evidence. (An earlier working draft mis-attributed this to Nature Sustainability.) https://www.nature.com/articles/s41599-024-04318-1

[13] Lupascu, M., et al. (2025). Half of land-use carbon emissions in Southeast Asia can be mitigated through the conservation and restoration of peat swamp forests and mangroves. Nature Communications. (~770 MtCO₂e/yr; ASEAN Peatland Management Strategy 2023–2030.) Peer-reviewed; 2025. https://www.nature.com/articles/s41467-025-55892-0

[14] ASEAN Climate Week 2026, Philippine DENR with UNDP and the ASEAN Secretariat; 27 April–1 May 2026; theme “From Ambition to Delivery.” Concluded late April 2026; not current week. https://www.undp.org/philippines/press-releases/philippines-lead-asean-member-states-advancing-climate-finance-and-policy-action-asean-climate-week-2026

[15] Asian Institute of Technology, regional webinar on nature-based solutions for climate adaptation and resilience in ASEAN cities (May 2026). No pipeline scale or financing model disclosed. https://ait.ac.th/2026/05/experts-discuss-nature-based-solutions-for-climate-adaptation-and-resilience-in-asean-cities/